2026 Federal Tax Guidelines: Updated Brackets and Standard Deduction

March 18, 2026

The IRS released updated tax brackets and standard deduction amounts for the 2026 tax year. Learn how these changes may impact planning for individuals and families.

Understanding the 2026 Federal Tax Updates

Each year, the IRS adjusts key parts of the tax code for inflation. These adjustments are designed to help prevent “bracket creep,” where taxpayers move into higher tax brackets simply because of rising prices rather than real increases in income.

For the 2026 tax year (filed in 2027), the IRS has released updated standard deduction amounts and income tax brackets, reflecting modest increases to keep pace with inflation.

While the underlying tax rates remain unchanged, the thresholds at which those rates apply have shifted slightly upward.

2026 Standard Deduction Amounts

The standard deduction reduces the amount of income subject to federal tax. Most taxpayers choose this option instead of itemizing deductions.

For tax year 2026, the standard deduction is:

- Single or Married Filing Separately: $16,100

- Married Filing Jointly: $32,200

- Head of Household: $24,150

These amounts represent a modest increase from 2025 levels and are intended to help offset the effects of inflation.

Additional deductions may apply for taxpayers who are age 65 or older or legally blind, which can further reduce taxable income.

For many households, the standard deduction alone significantly reduces taxable income before applying the tax brackets.

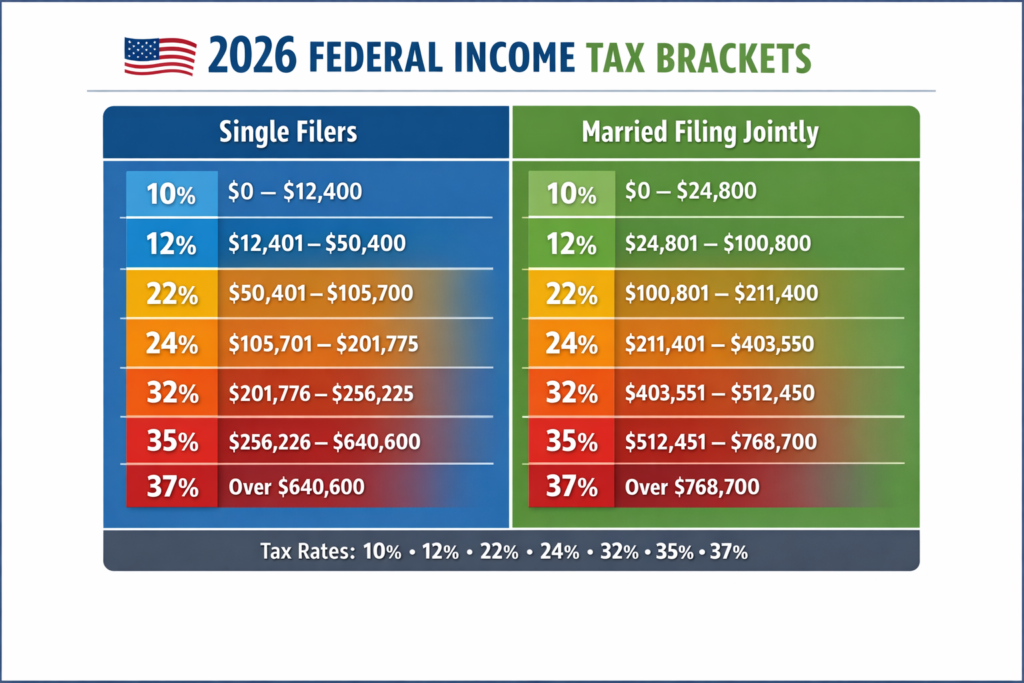

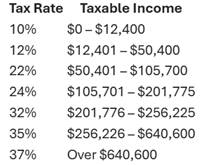

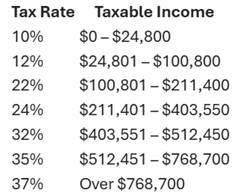

2026 Federal Income Tax Brackets

The United States uses a progressive tax system, meaning income is taxed in layers at increasing rates rather than at a single flat rate. Only the income that falls within each bracket is taxed at that bracket’s rate.

For 2026, the federal tax rates remain the same at 10%, 12%, 22%, 24%, 32%, 35%, and 37%, but the income thresholds have increased slightly.

Single Filers

Married Filing Jointly

These adjustments generally increase thresholds by roughly 2–3% compared with the prior year, reflecting inflation adjustments made by the IRS.

Why These Updates Matter for Planning

Even modest changes in deductions and brackets can influence financial planning decisions. Understanding the updated thresholds can help taxpayers:

- Estimate their potential tax liability more accurately

- Evaluate whether to take the standard deduction or itemize

- Consider timing strategies for income or deductions

- Coordinate retirement contributions and withdrawals

Because federal taxes are calculated based on taxable income after deductions, the standard deduction often plays a significant role in determining the final tax outcome.

Key Takeaways

For the 2026 tax year:

- The standard deduction increases to $16,100 for individuals and $32,200 for married couples filing jointly.

- Federal tax rates remain unchanged, but income thresholds have been adjusted upward for inflation.

- Understanding how deductions and brackets interact can help individuals and families plan more effectively.

Tax rules evolve regularly, and each taxpayer’s circumstances are unique. Staying informed about annual updates can help individuals make thoughtful financial decisions throughout the year.

Annual tax adjustments are designed to keep the system aligned with economic changes. While the updates for 2026 are relatively modest, they still affect how income is taxed and how deductions apply.

For individuals, business owners, and families thinking about long-term financial planning, understanding these changes is an important starting point for informed discussions with professional advisors.

The information provided is educational and general in nature and is not intended to be, nor should it be construed as, specific investment, tax, or legal advice.