Asset Allocation vs. Asset Location: What High-Net-Worth Families Need to Know

May 6, 2026

Learn the key differences between asset allocation and asset location and how each can play a role in building a more tax-aware, efficient investment strategy.

Asset Allocation vs. Asset Location: A Smarter Way to Structure Wealth

When it comes to building and preserving wealth, most investors are familiar with asset allocation—how investments are divided across stocks, bonds, and other asset classes. But a less discussed, yet equally important concept is asset location—where those investments are held.

For business owners, post-liquidity individuals, and multigenerational families, understanding the distinction between these two strategies can lead to more thoughtful, tax-aware portfolio design.

What Is Asset Allocation?

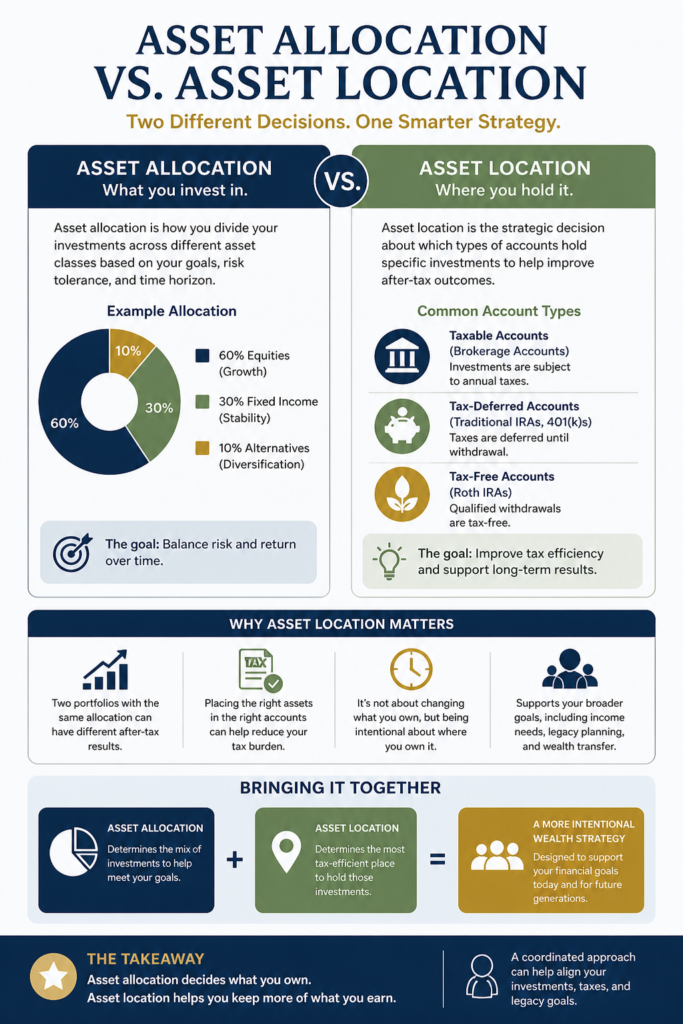

Asset allocation refers to how you distribute your investments across different asset classes based on your goals, risk tolerance, and time horizon.

For example, a simplified allocation might include:

- 60% equities for growth

- 30% fixed income for stability

- 10% alternatives for diversification

The purpose of asset allocation is to balance risk and return over time. It is one of the primary drivers of portfolio behavior during different market environments.

However, allocation alone does not address how efficiently those investments are structured from a tax perspective.

What Is Asset Location?

Asset location focuses on which types of accounts hold specific investments. These accounts typically fall into three categories:

- Taxable accounts (brokerage accounts)

- Tax-deferred accounts (e.g., traditional IRAs, 401(k)s)

- Tax-free accounts (e.g., Roth IRAs)

Each account type has different tax implications. Asset location aims to align investments with the most appropriate account type to improve after-tax outcomes over time.

Why Asset Location Matters

Two portfolios with identical asset allocations can produce different after-tax results depending on how assets are distributed across accounts.

For example:

- Interest-generating investments (like bonds) may be more tax-efficient in tax-deferred accounts

- Growth-oriented equities may be better suited for taxable or tax-free accounts, depending on the strategy

- Investments with higher turnover may benefit from tax-sheltered environments

The goal is not to change what you own—but to be intentional about where you own it.

Bringing Allocation and Location Together

Asset allocation and asset location are most effective when viewed together—not in isolation.

A well-structured portfolio often considers:

- Long-term growth objectives

- Liquidity needs

- Tax sensitivity

- Estate and legacy planning goals

For families managing significant or multi-generational wealth, this integrated approach can help align investment decisions with broader financial priorities.

Common Misconceptions

One common misconception is that asset location is only relevant for large portfolios. In reality, even modest levels of diversification across account types can create opportunities for more efficient structuring.

Another misconception is that asset location requires constant adjustments. In practice, it is typically implemented as part of a broader, disciplined strategy and revisited periodically as circumstances evolve.

A Practical Example

Consider an investor with:

- A taxable brokerage account

- A traditional IRA

- A Roth IRA

Instead of holding the same mix of investments in each account, a more intentional approach might involve:

- Placing tax-inefficient income-producing assets in the IRA

- Allocating long-term growth assets to the Roth IRA

- Using the taxable account for tax-aware equity exposure

While the overall allocation remains consistent, the structure becomes more aligned with tax considerations.

Asset allocation determines what you invest in. Asset location determines where you hold those investments. Both play distinct and complementary roles in portfolio construction.

For individuals and families navigating complex financial lives—especially following liquidity events or business transitions—these decisions can have meaningful long-term implications.

Taking a coordinated approach can help ensure that investment strategy, tax planning, and legacy goals are working in alignment.

If you’re thinking about how your investment structure aligns with your broader financial picture, a thoughtful review can be a valuable starting point. Omni 360 Advisors and Omni Legacy Law work with families and business owners to bring clarity and coordination to complex financial decisions.

This blog was developed with the assistance of AI-based tools for research, drafting and editing support (Chat GPT), and reviewed by OMNI 360 personnel for accuracy and relevance. The information provided is educational and general in nature and is not intended to be, nor should it be construed as, specific investment, tax, or legal advice.