Succession Planning Checklist for Business Owners and Families

June 8, 2026

Discover a practical succession planning checklist designed to help business owners and families prepare for leadership transitions, preserve legacy goals, and support long-term continuity.

For many business owners and families, succession planning is one of the most important — and often most delayed — aspects of long-term planning. Whether the goal is preserving a family enterprise, transitioning leadership, preparing for retirement, or creating continuity across generations, a thoughtful succession plan can help reduce uncertainty and support smoother transitions over time.

A well-structured succession plan is not simply about selecting a future leader. It also involves aligning legal, financial, operational, and family considerations in a coordinated way.

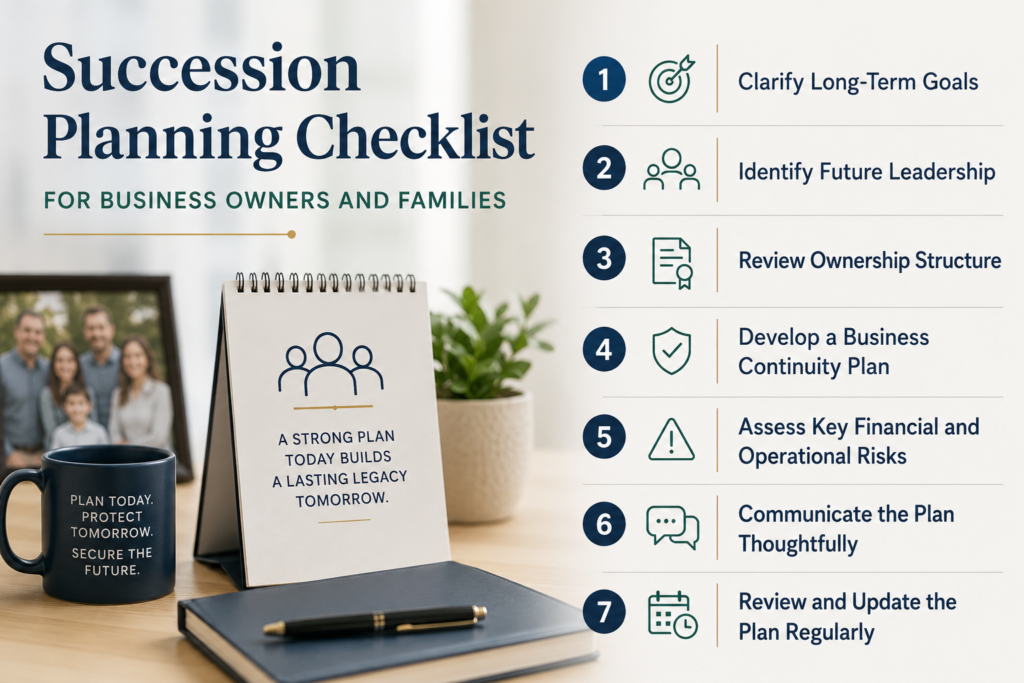

Below is a practical checklist to help guide the succession planning process.

1. Clarify Long-Term Goals

Before making technical or structural decisions, it is important to define the broader objectives of the transition.

Questions to consider include:

- Do you intend to keep the business in the family?

- Is a sale to a third party a future possibility?

- Should ownership and management remain together or be separated?

- What role do family members want to play in the future?

- What financial needs should the transition support?

Clear goals can help shape the structure of the plan and provide direction for future decisions.

2. Identify Future Leadership

One of the most visible components of succession planning is identifying who will assume leadership responsibilities over time.

Potential successors may include:

- Family members

- Existing executives or key employees

- External leadership candidates

- Strategic buyers or partners

Leadership readiness should be evaluated based on experience, communication skills, operational understanding, and long-term commitment to the organization’s vision and culture.

In many cases, a gradual transition period can help create continuity and provide mentoring opportunities for the next generation of leadership.

3. Review Ownership Structure

Succession planning should include a careful review of current ownership arrangements and transfer strategies.

Areas to evaluate may include:

- Shareholder or operating agreements

- Buy-sell agreements

- Voting and non-voting interests

- Trust structures

- Estate planning considerations

- Tax implications of ownership transfers

Coordinating legal and financial planning can help support continuity while addressing family and business priorities simultaneously.

4. Develop a Business Continuity Plan

Unexpected events can create operational challenges if responsibilities and decision-making processes are unclear.

A continuity plan may address:

- Interim leadership authority

- Key operational responsibilities

- Banking and financial access

- Client and vendor communication procedures

- Emergency decision-making protocols

Documenting these processes in advance can help the organization respond more effectively during periods of transition.

5. Assess Key Financial and Operational Risks

Succession planning should also include a review of the financial health and operational stability of the business.

Important considerations may include:

- Cash flow and liquidity needs

- Debt obligations

- Insurance coverage

- Key employee retention

- Customer concentration risk

- Technology and cybersecurity preparedness

Understanding these factors can help future leaders navigate transition periods more confidently.

6. Communicate the Plan Thoughtfully

Even well-designed succession plans can create confusion if expectations are not clearly communicated.

Open discussions with family members, business partners, and key employees can help:

- Reduce misunderstandings

- Clarify future roles

- Align expectations

- Support organizational stability

Communication strategies should be tailored to the needs and dynamics of the individuals involved.

7. Review and Update the Plan Regularly

Succession planning is not a one-time event. Businesses, families, and financial circumstances evolve over time.

Periodic reviews can help ensure the plan remains aligned with:

- Changes in business valuation

- Leadership development progress

- Family dynamics

- Tax and regulatory developments

- Long-term strategic goals

Many organizations benefit from reviewing succession plans annually or after significant life or business events.

A thoughtful succession plan can help business owners and families approach the future with greater clarity and organization. While every situation is unique, early planning often creates more flexibility and allows time for meaningful conversations and informed decision-making.

At Omni 360 Advisors and Omni Legacy Law, we believe succession planning works best when legal, financial, tax, and family considerations are viewed together as part of a coordinated long-term strategy.

This blog was developed with the assistance of AI-based tools for research, drafting and editing support (ChatGPT), and reviewed by OMNI 360 personnel for accuracy and relevance. The information provided is educational and general in nature and is not intended to be, nor should it be construed as, specific investment, tax, or legal advice.