The Financial Reality for Women After 65: Planning for Longevity, Income, and Legacy

May 7, 2026

Explore the unique financial challenges women face after age 65 and how coordinated tax, wealth, and estate planning can help support long-term security and legacy goals.

The Financial Reality for Women After 65

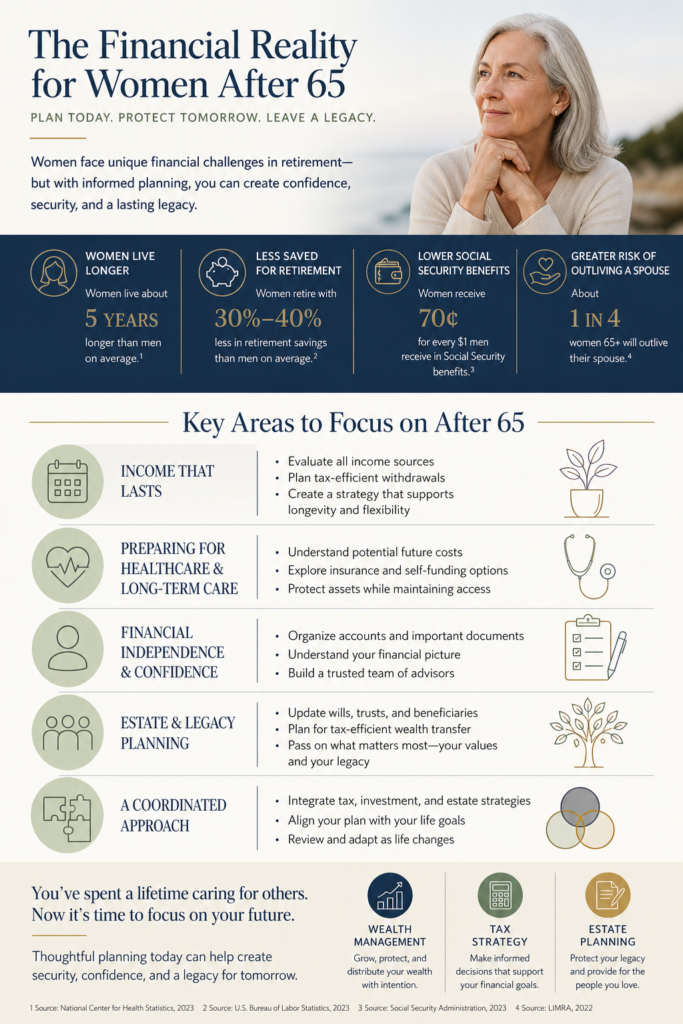

For many women, turning 65 marks not just a milestone birthday, but the beginning of a new financial chapter—one that often carries distinct challenges and considerations. Longer life expectancies, career interruptions, and evolving family roles can shape a very different retirement experience compared to their male counterparts.

Understanding these dynamics is essential for building a thoughtful, coordinated approach to tax planning, wealth management, and estate strategy.

Longevity: A Gift That Requires Planning

Women, on average, live longer than men. While longevity is certainly a positive, it also introduces a greater need for sustainable income over a longer period of time.

This extended timeline can place pressure on retirement assets, particularly when combined with:

- Lower lifetime earnings due to career breaks or wage disparities

- Reduced Social Security benefits

- Higher likelihood of outliving a spouse

A longer retirement horizon requires careful planning to help ensure that assets are structured to support income needs while also accounting for inflation, healthcare costs, and market variability.

Income Gaps and Retirement Readiness

Many women enter retirement with less accumulated wealth than men. This is often the result of time spent out of the workforce for caregiving, part-time employment, or delayed career progression.

As a result, key income sources—such as Social Security, pensions, and investment portfolios—may be more limited.

From a planning perspective, this makes it especially important to:

- Evaluate income sustainability under different scenarios

- Consider tax-efficient withdrawal strategies

- Align investment allocations with both income needs and risk tolerance

Thoughtful coordination between investment strategy and tax planning can play a meaningful role in helping extend the life of retirement assets.

Healthcare and Long-Term Care Considerations

Healthcare is one of the most significant financial variables in retirement, and women are statistically more likely to require long-term care at some point.

Planning for these potential costs involves more than simply setting aside funds. It may include:

- Evaluating insurance options or self-funding strategies

- Structuring assets to maintain flexibility and access

- Coordinating with estate plans to protect family intentions

These decisions are highly interconnected and benefit from a holistic approach that considers both financial and personal priorities.

The Transition to Financial Independence

Many women over 65 will, at some point, take on primary responsibility for financial decision-making—whether due to widowhood, divorce, or other life transitions.

This shift can be both empowering and complex.

Establishing clarity around financial accounts, income sources, estate documents, and trusted advisors is an important step in building confidence and continuity. A well-organized financial framework can help reduce uncertainty and support more informed decision-making over time.

Estate Planning and Legacy Intentions

Women often play a central role in shaping family legacy—both financially and personally. Estate planning is not just about transferring assets, but about expressing values, supporting future generations, and creating clarity for loved ones.

Key considerations may include:

- Updating wills, trusts, and beneficiary designations

- Planning for tax-efficient wealth transfer

- Incorporating charitable intentions or multigenerational planning strategies

Aligning estate plans with overall financial goals ensures that legacy intentions are carried out thoughtfully and efficiently.

A Coordinated Approach Matters

The financial realities women face after 65 are multifaceted. Income planning, tax strategy, investment management, healthcare considerations, and estate planning are deeply interconnected.

Rather than addressing these areas in isolation, a coordinated approach can help create greater alignment and clarity.

At Omni 360 Advisors and Omni Legacy Law, the focus is on helping individuals and families navigate these complexities through integrated planning—bringing together the legal, tax, and financial elements that shape long-term outcomes.

Retirement for women is not a one-size-fits-all experience. It is shaped by personal history, family dynamics, and evolving financial needs.

With thoughtful planning and a clear understanding of the challenges and opportunities ahead, it is possible to build a strategy that supports both financial stability and meaningful legacy outcomes.

If you’re beginning to think about these questions—or revisiting plans already in place—having the right framework and guidance can make a meaningful difference.

This blog was developed with the assistance of AI-based tools for research, drafting and editing support (ChatGPT), and reviewed by OMNI 360 personnel for accuracy and relevance. The information provided is educational and general in nature and is not intended to be, nor should it be construed as, specific investment, tax, or legal advice.